Understanding Home Loan Types: Which One is Right for You?

When navigating the world of home loans, it's essential to understand the various types available to find the one that best suits your financial situation and goals. The most common categories include fixed-rate mortgages, where the interest rate remains the same throughout the loan term, and adjustable-rate mortgages (ARMs), which start with a lower initial rate that may fluctuate over time. Other options include interest-only loans, where you pay only interest for a set period, and government-backed loans, such as FHA and VA loans, designed to help first-time buyers or eligible veterans access affordable housing.

To determine which home loan type is right for you, consider your financial stability, how long you plan to stay in the house, and your tolerance for risk. If you prefer stability and plan to stay long-term, a fixed-rate mortgage might be the best choice. Conversely, if you're open to potential changes in your interest rate or are looking to relocate in a few years, an adjustable-rate mortgage could save you money initially. Always evaluate your options carefully, and consult with a mortgage professional to ensure you make an informed decision.

Decoding the Home Loan Process: Steps to Secure Your Mortgage

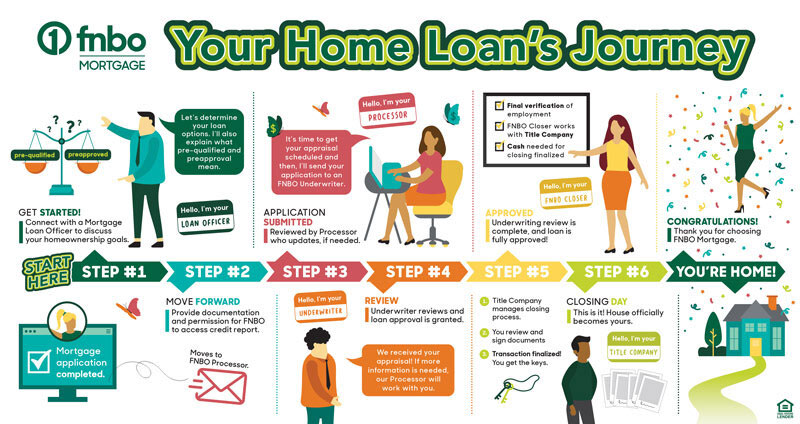

Understanding the home loan process is crucial for anyone looking to secure a mortgage. The journey typically begins with pre-approval, where lenders assess your financial situation to determine how much you can borrow. This involves providing documentation such as income statements, tax returns, and credit reports. Once pre-approved, you can confidently shop for homes within your budget, knowing the price range you can afford. It's also important to compare different lenders and mortgage products, as interest rates and terms can vary significantly.

After finding the right property, the next step is to submit a mortgage application. During this phase, your lender will perform a thorough review of your financial background and the property you wish to purchase. A critical part of this process is the appraisal, which ensures that the property value aligns with the loan amount. If all goes well, you'll receive a loan estimate detailing your monthly payments, interest rates, and closing costs. Finally, upon approval, you'll move towards the closing stage, where legal documents are signed, and the keys to your new home are handed over!

Common Myths About Home Loans: What You Need to Know Before Applying

When it comes to obtaining a home loan, many potential buyers fall prey to common myths that can skew their understanding of the process. One prevalent myth is that you must have a 20% down payment to secure a mortgage. This misconception can deter many first-time homebuyers, who may believe they are unable to afford a home. In reality, there are various loan options available, including FHA loans, which allow for down payments as low as 3.5%, making home ownership accessible to a broader demographic.

Another widespread myth is the belief that a perfect credit score is mandatory for getting a home loan. While a higher credit score can improve your chances of getting approved and securing better interest rates, it is not the only factor lenders consider. Many lenders offer programs tailored for those with less-than-perfect credit, and demonstrating a reliable income and solid payment history can often compensate for a lower credit score. Understanding these myths is crucial for anyone looking to navigate the home loan landscape successfully.